Notifications

Posted by supriya maximize

Filed in Business 207 view

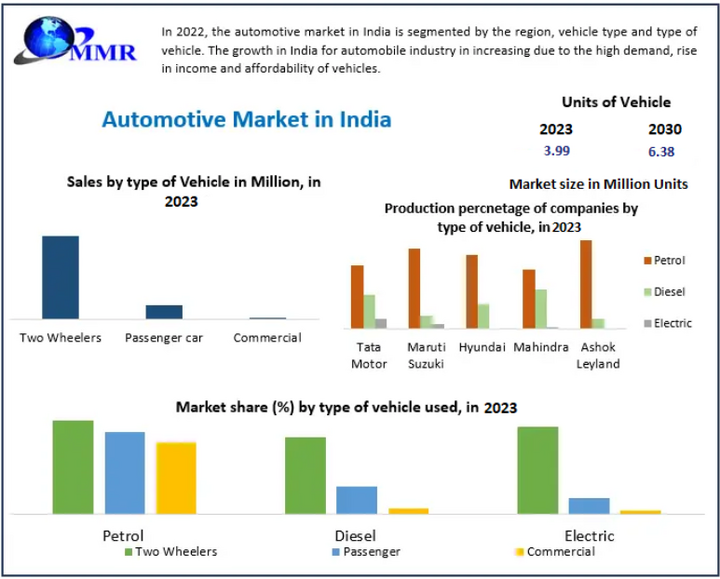

The Automotive Market in India reached 3.99 million units in 2023 and is projected to hit 6.38 million units by 2030, expanding at a CAGR of 6.94%. As one of the world’s fastest-growing mobility ecosystems, India’s automotive sector continues to evolve through electrification, policy reforms, export expansion, and rising consumer aspirations.

The automotive industry in India encompasses the manufacturing, distribution, and sales of vehicles spanning two-wheelers, passenger cars, commercial vehicles, and three-wheelers. India’s dominance is driven by:

A growing young population

Rising disposable incomes

Rapid urbanization

Supportive government policies

Demand for affordable and fuel-efficient vehicles

Automakers are steadily shifting toward EVs, connected vehicles, and advanced safety systems, which are reshaping the competitive landscape. Strong R&D participation—both domestic and global—continues to enhance innovation capabilities.

Find out where the real opportunities lie! Get your free report sample today by clicking here:https://www.maximizemarketresearch.com/request-sample/86126/

India’s expanding middle-class population and increasing workforce participation remain core growth accelerators. According to SIAM, over 1.69 million vehicles were produced in June 2021 alone, reflecting the sector’s strong production recovery post-pandemic.

Key Growth Drivers:

Rise in income levels and lifestyle upgrades

Demand for safer, more comfortable mobility solutions

Increasing exports (1.41 million units shipped between April–June 2021)

Booming digital retail and financing ecosystem

Government initiatives—such as FAME II, PLI scheme for the auto sector, and promotion of hybrid and electric vehicles—continue to support long-term transformation.

Despite its growth momentum, the industry faces substantial challenges:

High pollution levels in major cities pushing stricter emission norms

Rising production costs due to mandatory safety and emission upgrades

High manufacturing cost for EV batteries, sensors, ADAS & autonomous systems

Frequent regulatory revisions affecting production efficiency

Road infrastructure gaps, especially in rural regions

The cost of adopting cutting-edge technology continues to limit mass-scale implementation across all vehicle categories.

India is emerging as a global automotive R&D hub. Key developments include:

Government push through Make in India, Atmanirbhar Bharat and Automotive Mission Plan 2016–2026

Strong foreign investments for local production and component manufacturing

India accounting for 40% of global engineering and R&D spending (SIAM)

Rapid development in connected vehicles, telematics, autonomous features

Increased EV development boosting demand for wiring harnesses, sensors, batteries, and semiconductors

This innovation-led environment is strengthening India’s position in the global automotive value chain.

India’s worsening air quality—especially in cities like Delhi—has made EV adoption a necessity rather than a choice. Government measures include:

Lower GST on EVs

Strict BS6 emission standards

Incentives for EV buyers and manufacturers

Promotion of hybrid and electrified powertrains

With India becoming the world’s most populous country, traffic congestion and pollution concerns are expected to continue driving the electric mobility transition.

Two-wheelers account for the largest share due to:

Affordability

Fuel efficiency

Ease of mobility in congested cities

Suitability for both rural and urban terrain

Top players: Hero MotoCorp, Honda, Bajaj, TVS

Motorcycles lead demand, followed by scooters and mopeds.

Growth driven by:

Urbanization

Increasing working population

Financing availability

Rising preference for safety and comfort

Popular vehicle types: Hatchbacks, Sedans, SUVs, MPVs/MUVs

Growth supported by:

Expanding logistics & infrastructure

Increasing e-commerce penetration

Large-scale industrial and agricultural transport needs

Key players: Tata Motors, Ashok Leyland, Mahindra

Most affordable category

Widely available infrastructure

Higher popularity in small passenger cars and two-wheelers

Preferred for:

Heavy-duty applications

Long-distance travel

Trucks, buses, commercial fleets

Driven by:

Government incentives

Environmental concerns

Improving charging infrastructure

Fall in battery prices

Find out where the real opportunities lie! Get your free report sample today by clicking here:https://www.maximizemarketresearch.com/request-sample/86126/

High population density

Rapid urbanization

Strong demand for two-wheelers and SUVs

Expanding commercial vehicle adoption

Large agricultural footprint

Proximity to major ports (Mumbai, Kandla)

High demand for luxury cars

Rising infrastructure investments

Strong middle-class base

High 2-wheeler penetration

Strong IT ecosystem boosting automotive digitization

High demand for hatchbacks, SUVs, and rental fleets

Hilly terrain limiting mobility

Demand mainly in selective plain regions (Assam, Nagaland)

Growing two-wheeler usage for basic mobility

India’s automotive market is highly competitive with a mix of global and domestic giants.

Tata Motors Ltd – leader in passenger & electric cars; strong export presence

Maruti Suzuki India Ltd – mass-market leader; large-scale expansion in Haryana

Mahindra & Mahindra Ltd – strong SUV & EV brand

Hero MotoCorp, Honda, Bajaj, TVS – two-wheeler giants

Ashok Leyland, Eicher Motors – leaders in commercial vehicles

Hyundai Motor India, Toyota, Volkswagen – strong passenger car presence

Investments include:

Maruti Suzuki’s ₹18,000 crore manufacturing expansion

Hyundai’s ₹2,000 crore new HQ and facility upgrades

Mahindra’s USD 403 million investment in EV manufacturing

Surge in EV and hybrid vehicle adoption

Expansion of connected and autonomous features

Growth in shared & subscription-based mobility

Increase in automotive exports

Strengthening domestic component manufacturing

Market to reach 6.38 million units by 2030

EV segment to grow at >30% CAGR

Two-wheelers to remain dominant

SUVs to continue leading passenger car sales

The Automotive Market in India is undergoing a major transformation driven by innovation, policy reforms, electrification, and rising consumer expectations. With strong domestic demand and increasing global interest, India is positioned to become one of the most influential automotive markets in the world by 2030.