الإشعارات

نشرت من supriya maximize

مصنفة في التكنولوجيا 4 مشاهد

Global Underground Mining Vehicles Market: Electrification, Innovation, and Sustainability Driving the Future of Mining

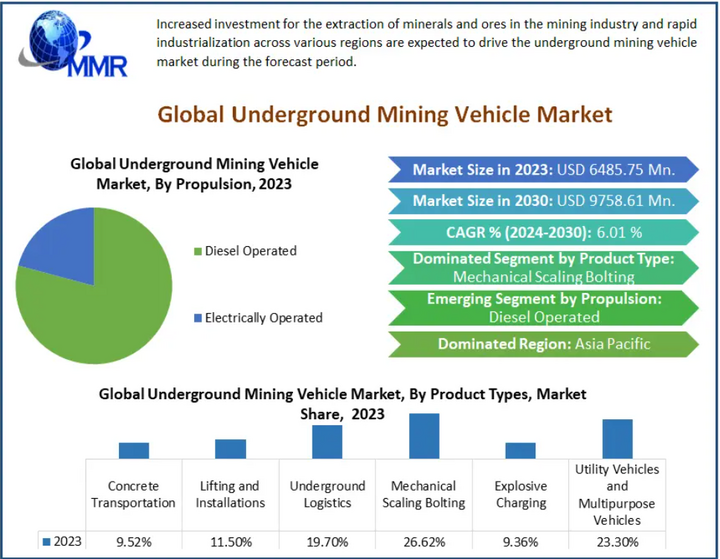

The Global Underground Mining Vehicles Market, valued at USD 6485.75 million in 2023, is projected to reach USD 9758.61 million by 2030, expanding at a CAGR of 6.01% during the forecast period (2024–2030). The market’s evolution is being powered by the growing demand for minerals and metals, coupled with the industry’s strategic pivot toward sustainability, automation, and electrification.

To know the most attractive segments, click here for a free sample of the report:https://www.maximizemarketresearch.com/request-sample/121278/

Underground Mining Vehicles (UMVs) form the backbone of modern underground mining operations. These machines—ranging from loaders and trucks to utility and service vehicles—are engineered to perform under the harshest and most confined environments. They enable efficient transportation, maintenance, and production support in underground mines while ensuring the safety and productivity of workers.

With the global drive toward renewable energy technologies, the demand for critical minerals such as lithium, nickel, and cobalt has surged, directly fueling the need for advanced underground mining equipment.

The mining industry is transitioning rapidly toward all-electric fleets, a trend expected to revolutionize underground operations. Electrification not only reduces carbon emissions but also enhances safety by minimizing diesel exhaust in poorly ventilated environments.

Companies like Normet are leading the charge with their SmartDrive electric equipment, designed to optimize performance and sustainability. Similarly, Caterpillar, Epiroc, and Komatsu are expanding their electric and hydrogen-powered vehicle portfolios to meet the growing sustainability standards across global mining operations.

Automation, digitalization, and energy-efficient technologies are reshaping underground mining. Innovations such as Sandvik’s AutoMine Fleet automation system and Epiroc’s battery-electric trolley truck systems are redefining operational efficiency and safety.

For example, Sandvik’s SEK 345 million deal with Hindustan Zinc in 2024 underscores the industry’s increasing reliance on automation and digital mining solutions. Similarly, MacLean Engineering’s new BEVs are driving reductions in energy costs while enhancing ventilation efficiency in underground environments.

With the mining sector contributing approximately 4–7% of global greenhouse gas emissions, sustainability has become a central priority. OEMs are increasingly developing low-emission and energy-efficient vehicles, focusing on electrification and alternative fuel sources. The GM-Komatsu collaboration on hydrogen fuel cell-powered trucks represents a groundbreaking step toward zero-emission mining.

Diesel Operated (79.17% share in 2023): Preferred for their durability, torque, and extended operational range, diesel vehicles continue to dominate large-scale mining operations.

Electric Operated (20.83% share in 2023): A rapidly growing segment driven by stricter emission norms and technological advancements in battery and charging infrastructure.

Concrete Transportation: Agitators, Transmixers, and others

Lifting and Installations: Scissor Lifts, Multi-Lifts, Boom Lifts

Underground Logistics: Crane Machines, Fuel Lube Trucks, Flat Decks

Mechanical Scaling and Bolting: Bolters, Scalers, Shotcrete Machines

Explosive Charging, Utility, and Multipurpose Vehicles: Graders, Cassette Trucks, and others

To know the most attractive segments, click here for a free sample of the report:https://www.maximizemarketresearch.com/request-sample/121278/

Asia Pacific (34.45% Market Share, 2023):

Dominates the global market, driven by large-scale mining in China and Australia. Heavy investments in advanced and automated mining equipment fuel growth in this region.

North America (27.31% Market Share):

The U.S. and Canada are adopting electric and autonomous mining vehicles to enhance operational efficiency and meet stringent safety standards.

Europe (22.01% Market Share):

Leading the shift toward cleaner mining technologies, with Sweden, Finland, and Germany focusing on battery-electric vehicles and sustainable mining initiatives.

South America & MEA:

Emerging opportunities due to the region’s rich mineral deposits and growing investments in modern mining infrastructure, particularly in Brazil and South Africa.

The market is highly competitive and innovation-driven, with global players focusing on sustainability, automation, and expansion through partnerships and acquisitions.

Key Developments:

May 2024: Sandvik secures SEK 345 million order from Hindustan Zinc, enhancing its stronghold in the Indian mining sector.

January 2024: Caterpillar unveils its first battery-electric underground truck in collaboration with Newmont, advancing electric haul solutions.

December 2023: GM and Komatsu announce a hydrogen fuel cell-powered mining truck project, pioneering zero-emission heavy-duty equipment.

March 2023: MacLean Engineering launches three BEVs—ML5, MC5, and BT5—enhancing underground mine safety and efficiency.

Aramine

Caterpillar Inc.

Epiroc AB

Komatsu

Sandvik AB

Normet

MacLean Engineering

Getman Corporation

GHH Group

BEML Limited

Fermel (Pty) Ltd

Dieci Srl

Dux Machinery Corporation

J.H. Fletcher & Co.

Beijing Anchises Technology Co., Ltd

The Underground Mining Vehicles Market is entering a transformative phase, driven by electrification, sustainability, and digital innovation. As mining companies transition toward low-emission operations, demand for battery-electric and hydrogen-powered vehicles is set to surge. With Asia Pacific leading the charge and North America and Europe following suit, the next decade promises a cleaner, smarter, and safer underground mining future.